Bigger. Better. Bolder. Inman Connect is heading to San Diego. Join thousands of real estate pros, connect with the Inman Community, and gain insights from hundreds of leading minds shaping the industry. If you’re ready to grow your business and invest in yourself, this is where you need to be. Go BIG in San Diego!

Mortgage giant Fannie Mae is turning to controversial Silicon Valley data analytics company Palantir Technologies to help it detect mortgage fraud, which the head of its federal regulator, Bill Pulte, claims is “rampant.”

Palantir’s “cutting edge AI technology” will help Fannie Mae find criminals who try to defraud it, increasing safety and soundness “by rooting out bad actors in our housing system,” Pulte said in announcing the partnership Wednesday.

TAKE THE INMAN INTEL INDEX SURVEY FOR MAY

As President Trump’s appointee to lead the Federal Housing Finance Agency (FHFA), Pulte last month sent a criminal referral letter to the U.S. Department of Justice suggesting that New York Attorney General Letitia James had made misrepresentations about two properties she owns in order to receive better loan terms.

James — who won a $486 million civil fraud judgment against Trump that is under appeal — has denied the allegations, calling them baseless.

As FHFA director, Pulte appointed himself the chair of both Fannie Mae and its sister company, Freddie Mac, in March and has been highlighting mortgage fraud as an issue for the companies in recent public appearances.

Appearing on Donald Trump Jr.’s podcast, Triggered, last week, Pulte said he could not comment on James’ case.

Bill Pulte

“But I will say that people claiming that they live in certain states that they don’t live in, people claiming other representations that are maybe not necessarily true — these are very big concerns to the mortgage market,” Pulte said. “It doesn’t matter whether you’re a welder, a plumber, a politician, an attorney — if you commit mortgage fraud, you are a risk to the system.”

In his criminal referral, Pulte claimed James falsified records by stating that a Norfolk, Virginia, home she purchased with her niece was to be her principal residence, the New York Post reported. Separately, Pulte accused James of misrepresenting the number of units in her Brooklyn residence to obtain better loan terms.

“Occupancy fraud is a huge issue in the country where people are basically getting loans based on certain down payments and certain interest rates, based on saying that they live in one area and not another, as well as saying that they should qualify for loans that maybe they shouldn’t have,” Pulte told Trump Jr. “So, you know, just generally speaking, my thought is that mortgage fraud is rampant and we are doing everything we can. We’ve made a number of criminal referrals — not just [James] — and we will continue to prosecute.”

Letitia James

James has acknowledged a clerical error on a 2023 power of attorney form related to the purchase of the Virginia property, but denies wrongdoing.

“This investigation into me is nothing more than retribution,” James told the Post.

Palantir’s business booming under Trump

Palantir has a long history as a government contractor, providing services to a range of federal agencies including the IRS, the National Institutes of Health and the Department of Veterans Affairs that generated $1.2 billion in revenue last year. During the first quarter of 2025, new defense contracts helped the company grow revenue from federal contracts by 45 percent from a year ago, to $373 million.

But Palantir has come under greater scrutiny during the Trump administration as it wins business that raises privacy concerns, such as an Immigration and Customs Enforcement (ICE) contract to build a platform that tracks the movements of immigrants.

A senior IRS official told CNN last month that employees at the agencies are concerned that Palantir is sifting through taxpayer data to track down immigrants and deport them.

Silicon Valley investor Paul Graham has accused Palantir of “building the infrastructure of the police state,” and demanded that the company make a public commitment that it will not build tools that could be used by the government to violate citizens’ rights, NPR reported this month.

“Palantir designs and deploys artificial intelligence and machine learning technology used by government agencies and commercial clients,” Fannie Mae said in a press release Wednesday. “The company’s technology provides expansive monitoring for anomalous transactions, activities, and behaviors to help companies detect suspicious activity and trigger investigative action.”

While Palantir co-founder Peter Thiel is a Trump supporter and donor, CEO Alex Karp is a Democratic donor who supported Kamala Harris for president, CNN noted.

Alex Karp

“This partnership with Fannie Mae will set off a revolution in how we combat mortgage fraud in this country,” Karp said in a statement. “We are bringing the fight directly to anyone who attempts to defraud our mortgage system and exploit hardworking Americans.”

How Fannie and Freddie deal with fraud

Fannie and Freddie don’t make loans themselves but buy mortgages from lenders and bundle them up into mortgage-backed securities (MBS) that are sold to investors. MBS are the ultimate source of funding for most U.S. home loans, and homebuyers enjoy low rates largely because the mortgage giants guarantee payments to investors.

Fannie Mae and Freddie Mac have the right to demand that lenders buy back mortgages if it’s later discovered that borrowers, sellers, real estate agents, lenders or appraisers made significant “misstatements, misrepresentations, or omissions” in selling loans to them.

Fannie and Freddie will only require lenders to buy back loans with misrepresentations when they identify a common pattern of activity on three or more loans made by the same lender. But there’s no such exemption for instances of fraud.

Fannie Mae specifies that it can require lenders to repurchase any mortgage where fraud is established in court or its investigators find “clear and convincing evidence” that a lender or other party “knowingly executed or participated in a scheme” to defraud it.

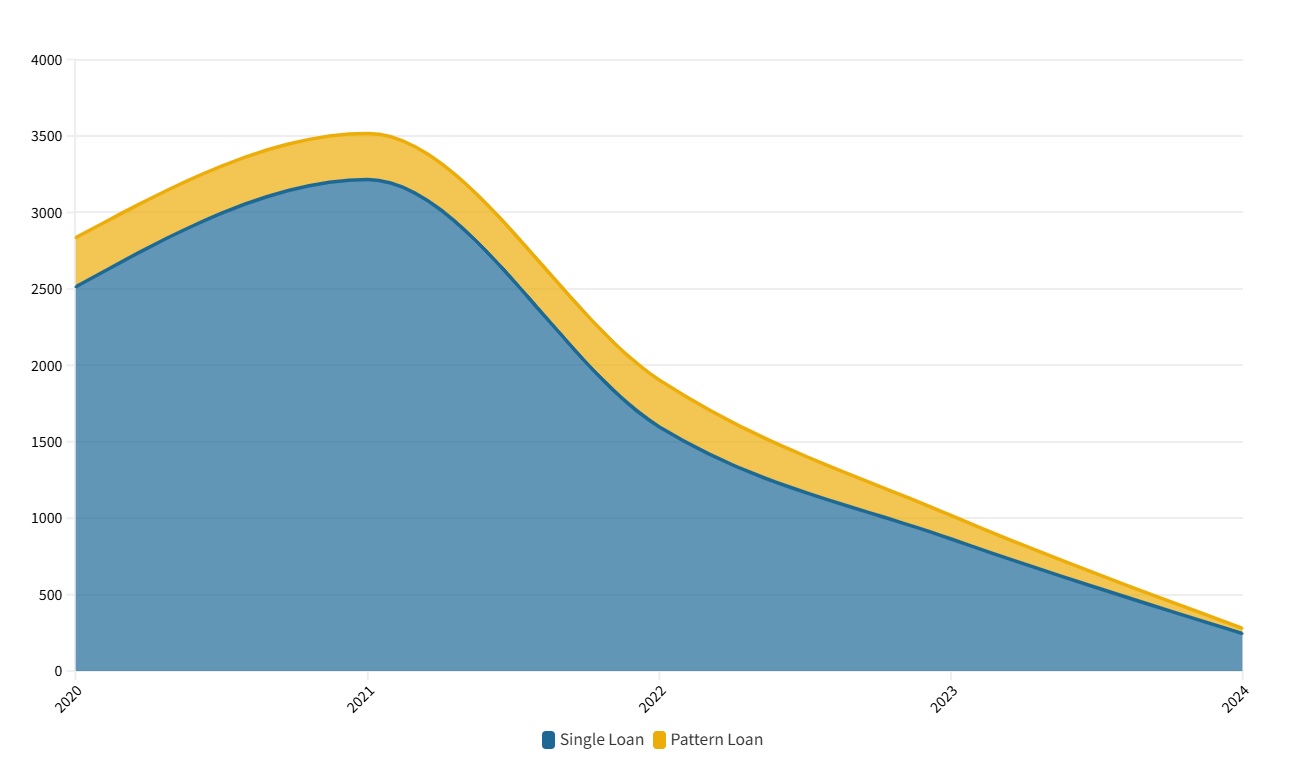

Fannie Mae fraud findings

Fraud findings on Fannie Mae-backed mortgages, 2020-2024. Source: Fannie Mae.

Mortgage fraud can go undetected for many years and is often discovered only when a borrower stops paying their loan.

So far, Fannie Mae’s Financial Crimes team has uncovered evidence of fraud in 3,517 single-family loans originated in 2021, including 3,215 single loans and 302 “pattern loans” — loans in which a common pattern of activity involving the same individual or company was discovered.

Through May 8, Fannie Mae investigators had uncovered evidence of fraud in only 280 loans originated last year — 245 single loans and 35 “pattern loans.”

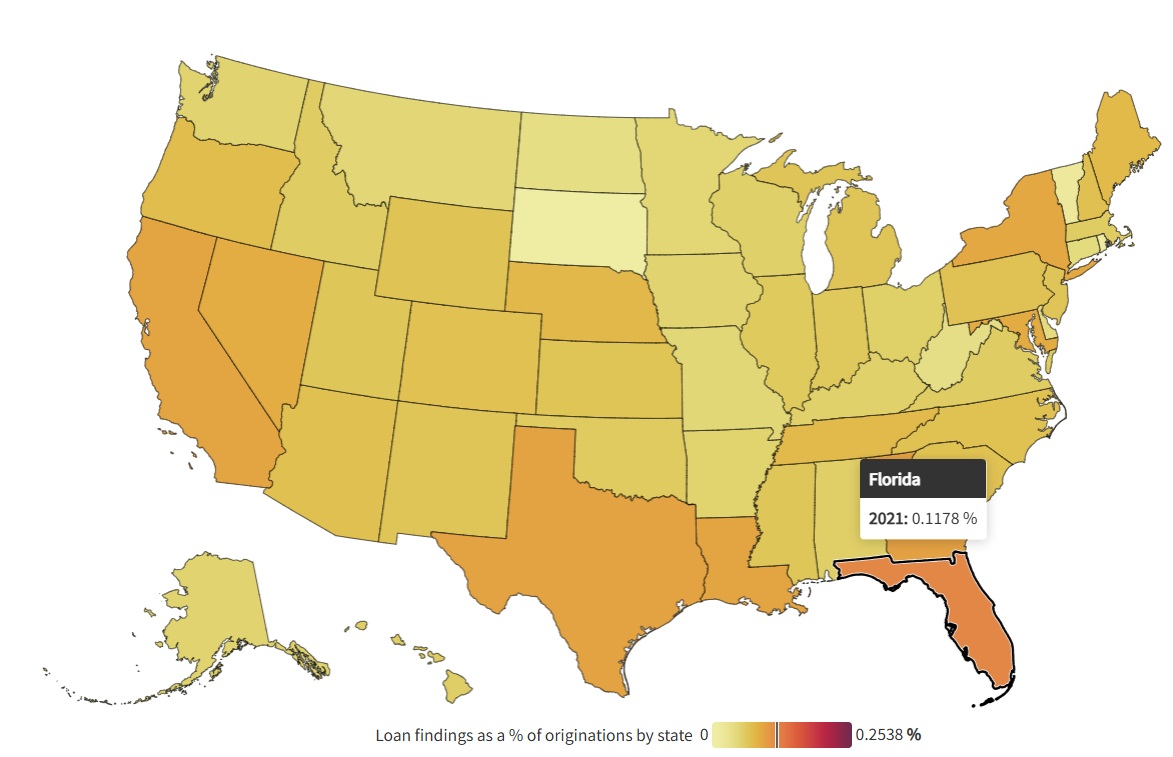

Loan fraud prevalence by state

Fraud as a percentage of Fannie Mae-backed loans originated in 2021 by state. Source: Fannie Mae.

With mortgage rates at historic lows, Fannie Mae in 2021 provided backing for 4.8 million single-family loans — 1.5 million purchase loans and 3.3 million refinancings.

In Florida, the state with the highest percentage of fraudulent loans, about 12 in 10,000 loans (0.12 percent) originated in 2021 were later found to have potential fraud issues.

In an October 2024 report, CoreLogic said about 1 in 123 mortgage applications lenders received in Q2 2024 showed indications of fraud, up 8 percent from a year ago. Fraud was more likely to show up in purchase applications (1 in 111) than in requests to refinance (1 in 171).

CoreLogic determined that New York, Florida, California, Connecticut and New Jersey are the states where lenders are at the highest risk for fraud.

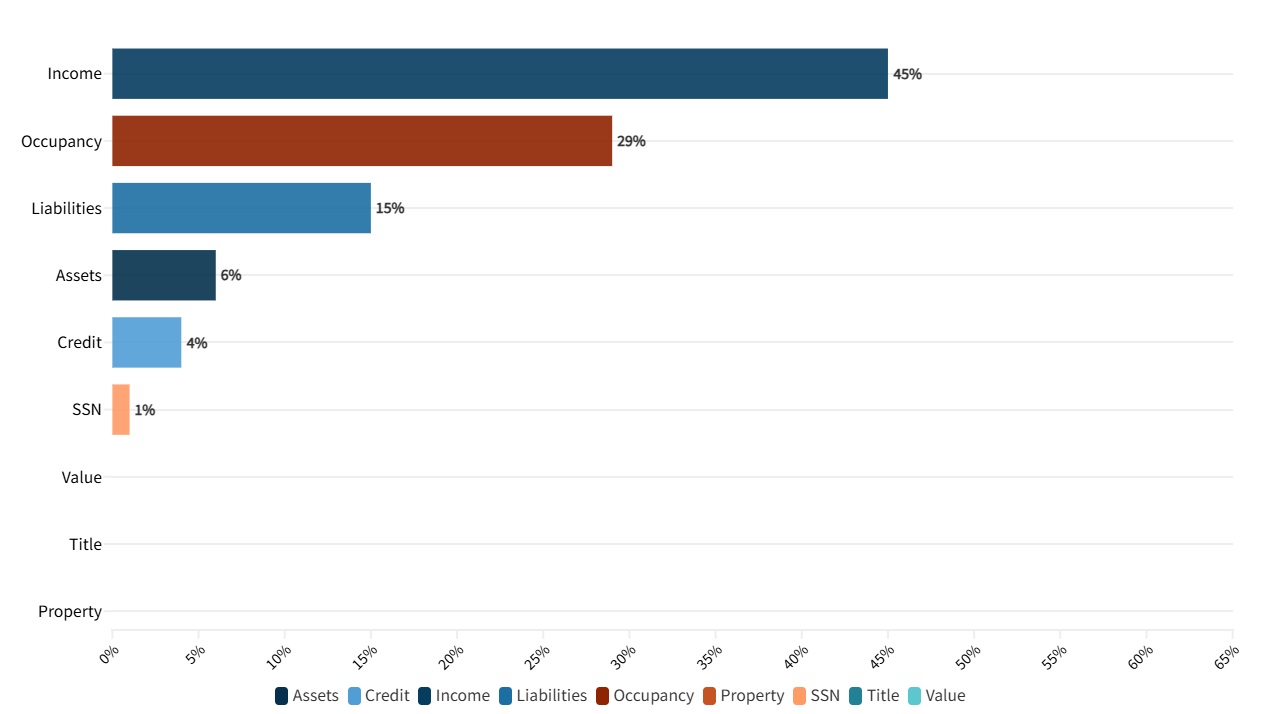

Most prevalent types of fraud

Types of fraud discovered on Fannie Mae-backed mortgages originated in 2024. Source: Fannie Mae.

Income misrepresentation was the most common type of fraud uncovered on loans backed by Fannie Mae last year (45 percent), followed by false occupancy claims (29 percent), understated liabilities (15 percent), overstated assets (6 percent), inflated credit (4 percent) and false social security numbers (1 percent).

Third-party mortgage brokers were blamed for much of the fraud that occurred in the subprime lending boom that preceded the 2007-2009 housing crash and Great Recession.

But mortgage brokers were involved in only about one in five Fannie Mae loans (19 percent) originated last year in which fraud is suspected, with third-party correspondent lenders involved with another 23 percent.

Most loans (58 percent) in which evidence of fraud was discovered were made by “non-third party” lenders like independent mortgage banks.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.